On June 23, a new rule was published that could put an end to the short squeeze madness we’ve seen throughout 2021.

The rule essentially allows the NSCC, which is one of the DTCC’s clearing firms, to check if a broker-dealer meets capital requirements more frequently.

To understand why this rule change matters, and how it might affect the short squeeze stocks like AMC Entertainment (AMC) and GameStop (GME), let’s put it into plain English.

New Rule Breakdown

Imagine your broker told you that you need to have at least $1,000 in your account to maintain good standing in your trading account. They will check on the first of every month, and as long as you have the money in your account on the first, you’re good.

So you can imagine that throughout the month, you might dip below that level a few times when you experience trading losses, but you’d be fine so long as the balance is at least $1,000 by the first of the month.

Now imagine your broker checking your account balance on a daily basis.

You’d have to change your operations, because now you can basically never dip below $1,000, because your broker is checking so often. So you might opt to trade with less capital, or deposit more into your trading account.

Either way, you can see how this rule change would influence your own behavior, so you can understand how this affects capital requirements for broker-dealers.

So, many of the traders involved in the GameStop (GME) and AMC Entertainment (AMC) short squeezes are betting that these rule changes will dramatically affect the ability of market makers and hedge funds to sell shares short, which they posit is putting downward pressure on the stock prices.

Keep in mind, there’s zero assurance that these theories are correct or incorrect. The rules have been in effect for two weeks now and we haven’t seen anything crazy happen yet, so the entire situation is still up in the air.

Why are capital requirements important?

Read on, we’ll get onto that once we explain some of the finer details of the rule.

What Is The Rule: New Rule for Market Makers Alters Capital Requirements

The new rule published by the NSCC is called SR-NSCC-2021-002, and it updates the calculation of a measure called Supplemental Liquidity Deposit, or SLD. The SLD is one of many benchmarks the NSCC uses to ensure that their members are liquid and able to meet settlement on their trades.

It’s essentially a formula that identifies higher-risk members that need to make additional deposits with the NSCC.

Prior to this rule change, the SLD was calculated once a month, around options expiration.

So, recall our example above, where your broker is checking your account balance once a month. The NSCC now calculates SLD each business day, and will even calculate it intraday where applicable.

This reduces the ‘wiggle room’ broker-dealers get with regard to NSCC capital requirements because they’re being checked up on more often.

Further, it also uses these higher-frequency snapshots to more closely observe member behavior in order to better calculate SLD, instead of using purely historical data.

Specifically, here are the three rule changes instituted by the NSCC in this amendment:

- calculating and collecting, when applicable, SLD each business day, rather than only during the monthly options settlement periods.

- calculating SLD based on observed Member activity, rather than based on historical and forecasted settlement activity.

- adopting an intraday SLD calculation and collection, when applicable, including on the first business day of the monthly options settlement periods based on additional exposures that are presented by options activity submitted after the start of day.

The NSCC and Capital Requirements

Let’s briefly get an understanding of why capital requirements are important.

Each brokerage firm needs to have a certain amount of cash on hand that is proportional to their operations. It’s kind of like fractional reserve banking. To ensure there’s not a liquidity crisis, the clearing house needs to ensure broker-dealers have adequate capital to pay for your trades.

This is called capital requirements and they’re enforced by the clearing houses, and clearing houses clear your trades, meaning they ensure sellers get paid and buyers get their securities by the settlement date.

It’s important to remember that clearing firms have to guarantee trades. If a member goes bankrupt, the clearing firm is essentially on the hook to make that member’s counterparty’s trades whole. So it’s very important that they have rigorous standards to protect themselves.

So, in short, capital requirements are important to clearing firms to:

- Ensure their members are liquid and can settle their trades without a problem

- Ensure their company is protected

Now, clearing and settlement aren’t exciting subjects and most people, including myself, aren’t experts. I’m not going to pretend like I’ve passed FINRA’s Compliance Officer Exam. So there’s a lot more to the clearing and settlement process than that.

But that’s the quick explanation you need to understand why this rule change is seen as very important to many retail investors.

To start, let’s get some background on the National Securities Clearing Corporation, the organization which is creating this rule.

Back in January 2021 when the first GameStop short squeeze occurred, it felt like the markets were broken.

There were rumors abound, and basically everyone was calling for some sort of regulatory fix. Short sellers were calling for regulation against Redditors, and the Redditors were calling for regulation on hedge funds and market makers.

In the heat of it, President Biden’s press secretary was getting several questions about GameStop each day, and Federal Reserve Chairman Jerome Powell was inundated with queries about the video game retailer at an FOMC conference that was meant to be about interest rates, unemployment, and the US economy.

Why Is the NSCC Suddenly Important?

The settlement process in financial markets is rarely a consideration to traders and investors. It’s viewed by many as a commoditized back-office role with little consequence to trading.

However, the short squeeze saga of 2021 brought the importance of settlement to the forefront.

Fingers were being pointed and people were a bit worried about potential cascading effects across the markets. Hedge funders pointed the finger at Reddit, and Reddit pointed it back at the hedge funds.

Both Fed Chairman Jerome Powell and President Biden’s Press Secretary were asked about GameStop several times, making for some quality entertainment.

On what other timeline is the President of the United States being asked about the store you bought your copy of Halo 3 in 2007?

Settlement got it’s heyday when Robinhood CEO Vlad Tenev suggested that US financial markets should migrate to a real-time settlement process, rather than the outdated T+2 settlement cycle we have now.

It was originally the DTCC’s $3 billion margin call against Robinhood and increased capital requirements on other brokerage firms that created all of the trading restrictions in the short squeeze stocks like GameStop (GME) and AMC Entertainment (AMC) back in January 2021.

Redditors involved in AMC and GME are now closely monitoring the movements of formerly ignored firms like the DTCC to better understand the market structure that created these short squeezes.

There are threads posted on subreddits like Superstonk and WallStreetBets with long discussions about the merits of new rules, and whether or not the AMC “Apes” should trust them.

From their point of view, the current equity market structure is unfair and enables short sellers to establish positions they otherwise wouldn’t be able to under a different settlement regime.

There are heaps of threads arguing these points on Reddit, so check them out as whatever we post here will likely be outdated by the time you read it.

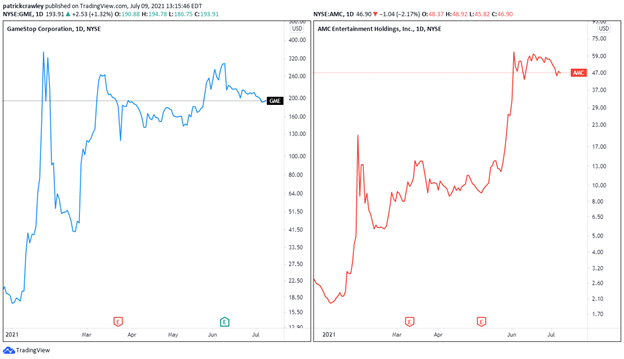

The Status of the GameStop (GME) and AMC Short Squeezes

While both AMC and GME are down significantly from their peaks, both stocks are holding up quite strongly considering both their ascent this year and their competitive positionings in their respective businesses.

And everyone has theories as to why they’re holding up.

It’s like a case of “to a man with only a hammer, everything looks like a nail.” Options traders are citing feedback loops in the options market, Redditors are citing short covering and peculiar market structure, and financial pundits are saying the word “Robinhood” a lot.

Final Thoughts

With this rule in the book for two trading weeks now, it’s difficult to determine the effect, if any. It’s always to draw conclusions just from watching price data about an event such as this because markets are so chaotic.

The clearing and settlement processes are still boring and confusing, but it’s a 100% positive that more people are paying attention to the nuts and bolts of how the market works by reading filings from the clearing houses.